Market Concentration: What’s really going on

If you've been following financial news lately, you've probably seen the headlines warning that the top 10 stocks now make up a larger share of major stock market indices than ever before. Most of these are technology and AI-driven companies, and if these giants stumble, the thinking goes, so will your portfolio.

It's a reasonable concern that we take seriously, but before rushing to make changes, it's worth examining what's actually happening beneath the surface.

These Aren't Really "10 Companies"

These aren't single businesses. They're conglomerates containing dozens of world-class operations that could easily stand alone as publicly listed companies.

Apple's AirPods division alone is thought to generate around $20 billion in annual revenue. If spun off tomorrow, it could be larger than Spotify, Nintendo, eBay, and Airbnb. Similarly, its Mac division, iPad division, and Wearables division would each rank among the world's largest technology companies if listed separately.

The same applies across the top 10. YouTube, buried inside Alphabet, generates $54 billion in revenue and would likely make it one of the 20 largest companies in the world. Amazon's AWS cloud division crossed $100 billion in revenue last year. Microsoft contains Azure, LinkedIn, Xbox, and Office 365, each generating billions independently.

The "top 10 concentration" is partly an illusion of corporate structure. If these companies reorganised into their component parts, the index would look far more diversified overnight, without any change in the underlying businesses you actually own.

Concentration Isn't New

Market leadership has always been concentrated. In the 1980s, it was oil companies and industrials. In 2000, it was the dot-com darlings, many of which no longer exist. The names at the top constantly change, but there's always a top 10 dominating returns.

What's different today is that these leaders have earned their position through actual revenue and profits, not speculation. The earnings generated by these companies justify much of their market weight. They sell real products to billions of real customers every day. This doesn't guarantee future success, but it's a more solid foundation than we've seen in previous concentration cycles.

The Index Self-Corrects

If these companies underperform, they will naturally become a smaller portion of the index. You're not locked in forever to today's winners.

Index investing is designed to automatically reduce your exposure to declining companies and increase exposure to rising ones. The next generation of market leaders, whatever they turn out to be, will gradually replace today's giants as their fortunes change. This process has played out countless times over the past century.

The Practical Question

Even if concentration does lead to higher risk or lower returns ahead, what's the alternative? Trying to predict which companies will decline? Moving to cash? Every alternative carries its own risks and usually involves speculation about an unknowable future.

We understand the concern, but when we look beneath the headlines, we find reasons for continued confidence in a diversified, long-term approach.

If you're investing for a decade or more, today's concentration is unlikely to determine your outcome. Staying diversified across thousands of companies remains the most sensible approach, even if a handful currently dominate the index.

As always, we're here if you'd like to discuss how this applies to your specific situation.

End of year checklist

As November progresses and the year begins its final act, thoughtful investors turn their attention to a different kind of preparation. While others are distracted by holiday planning and Black Friday sales, the financially literate consider whether there’s anything that needs tidying up in their financial life.

Most of the heavy lifting in financial planning happens in the big decisions you've likely already made. These small year-end actions separate good investors from great ones. They're the compound interest of good habits, the quiet discipline that results in peace of mind and financial security.

Before the year-end rush begins, here are five practical steps that deserve your attention in November.

Five Moves That Matter

The best investors know that great planning isn't built in dramatic moments but in consistent, thoughtful actions. Here are five year-end actions you can take to give you peace of mind during the holidays and help you to start 2026 on the right foot.

1. Review your insurance and beneficiaries.

November is the perfect time to check all your policies and accounts. The beneficiaries you named five years ago might not reflect your current wishes. On the slight chance that the insurer has made an administrative error, you’ll catch that too. This ten-minute review could save your family the headache of discovering an incorrect beneficiary nomination at claim stage.

2. Get your paperwork in order.

Nobody likes thinking about worst-case scenarios. Having your affairs in order brings peace of mind. Is your will current? Do your loved ones know where to find important documents? Think of this as creating a roadmap for those who might need it. Organisation today prevents chaos tomorrow. One afternoon of sorting could be the greatest gift you give your family.

3. Review your monthly subscriptions and debit orders.

Those small monthly payments have a sneaky way of multiplying. The streaming service you tried once, the gym membership you keep meaning to use, the insurance for the phone you replaced last year. Run through your bank statements and cancel what you're not using. You might be surprised how much you free up for next year's goals. Every dollar saved is a dollar that can work harder elsewhere.

4. Plan for major expenses.

Look ahead to 2026. What's coming that you already know about? A new car, home repairs, that memorable anniversary trip, children’s school fees? Identifying these expenses now allows you to prepare properly rather than scrambling later. Set up a separate savings pot for each major expense. When the time comes, you'll pay with satisfaction rather than stress.

5. That one thing you've been avoiding.

You know what it is. It could be consolidating old super pots, setting up that extra investment fund, or having the money conversation with your adult children. Whatever you've been putting off, November is your permission slip to tackle it. The relief you'll feel heading into the new year will far outweigh the discomfort of dealing with it now.

Small Actions, Big Impact

You don't need to tackle everything at once. Completing two or three of these items puts you ahead of most investors who let the year slip away without review. Choose the ones that resonate with your current situation and start there.

The fact that you're thinking about these matters while others are thinking only about upcoming Christmas lunches and shopping says something important about your financial maturity. You understand that small actions compound into significant results.

The financially literate don't need perfect execution. They need consistent attention to what matters. If you'd like help working through any of these year-end considerations, we're here to guide you.

Retirement Reimagined

Retirement as we know it is barely 150 years old. Otto von Bismarck introduced the world's first state pension in Germany in 1889, setting the retirement age at 70, an age that only a minority of the population actually reached.

The concept was simple: work until you could no longer physically do so, and then society would care for you in your final years.

That world no longer exists. The forces reshaping how we live and work are so fundamental that the retirement of the future is unlikely to resemble the retirement of the past. The question isn't whether retirement will change, but how quickly we can adapt our thinking to match this new reality.

For the first time in history, we have the tools and longevity to completely reimagine what the later decades of life could look like.

The Forces Reshaping Everything

Several powerful trends are making traditional retirement planning obsolete.

Longevity has exploded. Today's 65-year-old couple has a 50% chance that at least one spouse will live to 92. Today’s retirees are looking at 25 to 30-year retirements, not the 10-year periods our grandparents planned for.

Health spans are extending. People aren't just living longer, they're staying active much deeper into their lives. Many 70-year-olds today have the energy that 50-year-olds had a generation ago.

The workplace has been revolutionised. People change jobs every 4-5 years and switch careers multiple times. Remote work has made location independence possible for millions, and the gig economy enables flexible arrangements that were previously unimaginable.

Technology has eliminated barriers. You can work from anywhere, manage your life from your phone, and stay connected regardless of geography. The infrastructure that once tied us to specific locations has largely disappeared.

These changes are unlikely to be temporary. It’s more likely that they are permanent shifts requiring us to rethink how we structure our lives fundamentally.

What the Future of Retirement Could Look Like

The forces explored above mean that life no longer needs to follow the patterns of the past. Instead of working until 65 and then stopping completely, consider a more flexible approach that leverages these new realities.

While these possibilities were not an option for the previous generation, they will be options that future retirees will have the luxury to consider.

Periodic sabbaticals throughout your career. Take 3-6 month breaks every few years to recharge, pursue passions, or spend concentrated time with family. Remote work makes this increasingly feasible.

Strategic family time. Rather than missing your children's childhood, consider taking a year off when they're young to travel together or be fully present in their daily lives. Those memories can't be recaptured later.

Extended exploration periods. Take that year abroad at 45 when you have the energy to embrace the adventure. Test whether your retirement dreams match reality.

Shorter traditional retirement. By taking breaks throughout your life, you stay energised and can potentially work longer. Instead of 30 years of full retirement, work until 75 with a much shorter final retirement, having already lived many dreams along the way.

Those who take periodic breaks throughout their career may arrive at retirement with a much clearer vision of how they want to spend their later years than someone who worked nonstop for 40 years.

Planning for Multiple Possibilities

Research shows that we're not very good at knowing what our future selves will want. The only way to see how you'll feel about unstructured time, different locations, or various lifestyle arrangements is to test them.

For those who want to embrace the changing forces shaping our world, we have the following suggestions: Start small. Plan a two-month sabbatical. Try working remotely from a different city for a month. Experiment with part-time consulting in a field you're curious about.

More importantly, start building these possibilities into your financial planning. Instead of just saving for one big retirement, consider creating separate funds for periodic sabbaticals, location experiments, and extended family time. The monetary cost of these experiments is often much less than the lifetime value they provide.

If the future of retirement is expected to be more flexible, health-conscious, and globally connected, your financial plan should reflect these possibilities. We're here to help you align your investment strategy with whatever vision of the future most excites you.

It’s never too late

Have you ever looked at your financial situation and felt that familiar knot in your stomach? Maybe you've been putting off organising those scattered investment accounts, or you know your savings rate (the amount you invest each month) isn't where it should be. Perhaps you've glanced at a friend's retirement balance and wondered how you fell so far behind.

If this sounds familiar, you're not alone. We see this every day in our business. The good news is that it's never too late to improve your financial position. No matter where you are right now, a few focused improvements can transform your situation faster than you might imagine.

Getting in Shape

We suggest that you approach financial fitness the same way you'd approach physical fitness. You wouldn't expect to go from sitting on the couch to running a marathon overnight. That would be unrealistic and probably leave you injured or discouraged.

Instead, you'd start with small, manageable steps. You’d start with a 10-minute walk around the block. Then 15 minutes. Then, you’d add some stretching. Before long, those small actions compound into something significant.

Your finances work precisely the same way. The goal isn't to become perfect overnight. The goal is to start moving in the right direction and stay consistent. Small steps compound quickly when you stick with them. We make starting harder in our minds than it needs to be.

Keep Moving Forward

Sometimes work demands everything you have. Sometimes family needs take priority. Sometimes you're dealing with health issues or other challenges that push financial planning to the back burner.

That's completely normal. However, just because you've fallen behind doesn't mean you're stuck there permanently.

Fortunately, you don't need to overhaul your entire financial life in one weekend. You need to take the next right step. Even small actions create forward movement.

Remember, slow progress beats no progress every time. The person who saves an extra $100 per month for five years will be in a dramatically different position than the person who kept meaning to "get organised" but never started.

Your Seasons of Improvement

We see a common pattern with our clients. They make a few improvements, let those changes settle in, then tackle the next area.

You might start by consolidating those old pension accounts scattered across previous employers. This simple step often reduces fees and makes your investments easier to monitor. Once that's organised, you might increase your monthly savings by setting up an automatic transfer. After that becomes routine, perhaps you review your investment allocation.

These aren't dramatic changes, but they add up quickly. When you consolidate accounts and create clear systems, you gain mental clarity. You start to feel "caught up" rather than constantly behind. This confidence often motivates further improvements.

Your Journey Forward

We've learned from working with many families that a few short seasons of focused improvement can completely transform your financial position. We've seen people go from feeling hopeless about retirement to feeling confident about their future, often in just two to three years.

If you're feeling behind or overwhelmed, take heart. Small, consistent actions compound faster than you expect. The next few years could look dramatically different if you start moving forward today.

We're here to guide you through this process. Whether you need help consolidating accounts, increasing your savings rate, or getting organised, we can show you the way forward. The first step is often the hardest, but it's also the most important. Are you ready to take it?

The courage to feel left out

You've probably heard a few stories of investors who made a fortune with a single investment decision. The neighbour who bought Amazon early and saw massive returns, or the colleague who invested in AI startups and is now talking about early retirement.

When we hear stories like these, it's natural to feel like we're being left out. However, for every success story you hear, there are countless others you don't. Families who chased the next big thing, only to watch significant capital disappear when they backed the wrong company or the hype faded.

Every new technology and industry will lead to incredible success stories for some investors. However, for long-term investors to risk the family financial fortress on isolated bets is irresponsible.

While it makes sense to have some exposure to sectors driving our future, every successful investor must become comfortable with feeling under-allocated to the hottest trends.

We strongly believe that every wise investor needs to have the courage to feel left out.

Hidden in Plain Sight

Here's the irony: You likely already own the companies you think you're missing out on.

That Amazon stock your neighbour keeps bragging about? It's sitting in your global equity portfolio right now. Those AI companies making headlines? Your diversified funds likely hold shares in some of them.

But here's why it doesn't feel that way. When you own a stock directly, every price movement becomes personal. You track it regularly, feel each rise and fall, and own the story along with the shares. The dopamine rush is real and addictive.

When you own a stock through a fund, it's hidden among hundreds of other holdings. No daily drama, no emotional highs and lows, no story to tell at parties. Just steady participation in whatever growth occurs.

Our brains crave the excitement of individual ownership, even though the diversified approach often delivers better results. We want to feel like active participants, not passive beneficiaries.

Mature investors recognise this psychological gap and embrace it. They know they're not actually missing out. They're participating more intelligently.

Time-Tested Wisdom

Since you already participate in the winners through diversification, the question becomes: should you stick with this proven method or complicate it by chasing individual opportunities?

This brings us to a fundamental choice every investor faces. You can focus on what has always worked, or you can focus on what's working now. Mature investors choose the former. Those chasing returns get distracted by the latter.

What has always worked? Global equities have consistently rewarded patient investors across every technological shift. Whether it was railways, electricity, automobiles, computers, or the internet, the great companies adapted and thrived. The businesses that couldn't adapt were replaced by those that could.

Your diversified portfolio captures this innovation without requiring you to guess which specific companies will lead the next wave of innovation. You benefit from human ingenuity and progress without the stress of picking winners.

Every generation believes its current investment opportunity is different and revolutionary. The fundamentals of business growth and compound returns remain constant, even as the headlines change.

Mature investors understand that what feels exciting today will likely be tomorrow's forgotten fad. They choose time-tested wisdom over trendy speculation.

Your Perfect Position

If you're between 40 and 55, you're perfectly positioned to embrace this time-tested approach. You have both the time horizon and the life experience to choose wisdom over excitement.

Your 10 to 25 years until retirement means steady returns are more than enough for financial independence. You don't need to swing for the fences. Your peak earning years allow you to save consistently, and your time horizon enables you to weather temporary volatility.

More importantly, you have the maturity to see through the hype cycles. You've lived through enough "revolutionary" investment opportunities to recognise the pattern. You understand that what feels urgent and exciting today rarely has a lasting impact on long-term wealth building.

This combination of time and wisdom puts you in the sweet spot. You can choose to be content with feeling left out while others chase the latest trends. You can focus on what has always worked while others get distracted by what's working now.

Your future self will thank you for having the courage to stay invested in proven fundamentals rather than speculative bets. We're here to help you maintain this discipline. Sometimes the most courageous thing you can do is nothing at all.

Know your numbers

The road to financial freedom is a journey of a thousand steps. Fortunately, the path is well-trodden by millions of investors who have already reached financial independence. From their experience and our experience advising many such clients, we can extract the key learnings and metrics you’ll need as you continue your financial journey.

This journey is a marathon, not a sprint. It will require patience, discipline, optimism, and regular reflection on where you are in the process. It is this practice of measuring your progress that we want to reflect on today so that you can avoid the fate of too many unsuccessful investors: discovering an unpleasant truth when it’s too late to correct course.

The Road To Failure

While successful investors have many common traits that we can learn from, so do those who were unsuccessful in their quest. Common mistakes of those who fail are insufficient contributions, incorrect investment portfolio decisions, acting on emotion, and inadequate protection.

However, perhaps the trait that leads to all the mentioned mistakes is the failure to take regular stock of their reality, preventing them from making changes that could rescue their situation.

Like flying, financial planning is not a perfect science. The assumptions we make about the future are sure to be incorrect, but they’re useful all the same. This requires us to be flexible, adaptive, and aware of our progress. Like flying, a successful investing journey requires constant course corrections to arrive at the correct destination.

The Key Numbers

To make the right changes, you need to track the correct numbers. As the management expert Peter Drucker once said, “What gets measured, gets managed.” Below are the metrics we recommend you keep track of. By working with an adviser who understands how these numbers interact, we are confident that you, too, can reach financial freedom.

Your wealth window – quite simply, how many months until you hit your financial independence day? This is when working becomes optional for you. Knowing this number in months rather than years makes it feel more motivating for most people. For example, if you’re 52 and want to retire at 62, you have 120 months left in your wealth creation window.

Your saving percentage - what percentage of your take-home pay are you investing for the future? The more you can put away, the faster you can retire. Additionally, by putting away more, you learn to live on less. Successful investors routinely save more than 20% of their income.

What percentage of your investments are in global equities - aka owning shares in the great companies of the world. Using history as our guide, equities provide the best long-term returns. Ideally, you want to continually move closer to a 100% allocation to equities, but the more, the better.

Your retirement income needs - how much monthly income will you require in retirement to live comfortably? This will depend on your lifestyle and aspirations.

Your retirement income shortfall – simply, the difference between what you will need and what your current expected retirement income is, possibly from a state pension or rental income. This is the number that your investment portfolio will need to provide. Your adviser will be able to help you understand how big your portfolio will need to be.

What percentage of your income is protected – this is what disability and life insurance is for. We all think we’re invincible, but this is a serious topic. Too many people insure their phones but not their income.

Review and Calibrate

From experience, we know that the more you know about your finances, the faster you can progress towards financial freedom. We encourage you to develop a system for keeping track of your progress across the areas outlined above.

Above all, knowing the truth about your situation gives you greater agency over the course of your future. Some people let life happen to them, and some shape their future to their desires. We encourage you to aspire to the latter.

Investor Discipline in the Digital Age

Have you noticed how difficult it is to escape the news cycle?

From breaking alerts on your phone to commentary filling your social media feed, world events now follow us everywhere. In this age of constant connectivity, information isn't just available but almost unavoidable.

There was a time, not so long ago, when investors might learn about market movements days after they occurred, reading about them in the morning newspaper at breakfast. Indeed, many successful investors built their wealth during an era when they might go an entire month without knowing how their investments were performing. This distance created a natural buffer against emotional decision-making.

However, times have changed.

The New Investment Environment

The contrast between yesterday's investment environment and today's couldn't be starker. What once required effort to discover now requires effort to avoid.

The financial media, competing for our attention, has discovered that anxiety and fear drive engagement. They've become remarkably efficient at transforming minor market fluctuations into seemingly urgent crises. "Markets in turmoil" has become the default headline, regardless of whether the decline is 2% or 10%.

Perhaps counterintuitively, research shows that having more information doesn't necessarily lead to better investment decisions. The human mind wasn't designed to process the volume of information we now receive. We're pattern-seeking creatures in a market that often presents random short-term movements. The cost is measurable: research shows that investors who trade frequently in response to news tend to underperform those who trade less.

Strategies for Today's Investor

How do we remain disciplined investors in this age of information abundance? Here are a few strategies that have proven effective for our clients:

Create intentional information boundaries. Consider checking your portfolio on a predetermined schedule rather than in response to headlines. For long-term investors, an annual review may be sufficient unless your circumstances have changed significantly. We see no benefit to checking your portfolio every week. As the saying goes, "The market is a device for transferring money from the impatient to the patient."

Focus on fundamentals, not prices. The true value of your investments lies in the earnings and dividends of the great companies of the world. During periods of market volatility, remind yourself that you own businesses, not stock tickers. Ask yourself: has the long-term outlook for these businesses fundamentally changed, or just their prices?

Remember your North Star. The most successful investors maintain a clear vision of why they're investing in the first place. For most investors, it's about their family's security and financial independence. During times of market turmoil, reconnecting with this purpose provides clarity that no headline can disrupt.

Taking Control

While the challenges of modern investing are real, the foundations of investment success remain unchanged. Regardless of the era, patience and discipline have always been the defining characteristics of successful investors.

It's worth remembering that we have tremendous power to shape our information environments. Despite living in a 24/7 news cycle, we are not obligated to participate in it. By turning off notifications, designating "news-free" days, or limiting financial media consumption, we can reclaim the mental space needed for thoughtful investment decisions.

As your financial advisers, we see our role not just as managers of your financial assets but as guardians of your peace of mind. We stand between you and the noise, helping you focus on what truly matters: your long-term financial well-being. In a world of increasing complexity, there's profound value in simplicity and staying the course.

Volatility - An investors friend

Investment markets have been very kind to global equity investors over the last two years. After a period of sideways markets and soaring inflation, the S&P 500 (the world’s premier stock market) rose by 24% in 2023 and another 23% in 2024.

With historical average returns in the 8-10% range, these are extraordinary returns that patient and disciplined investors will be delighted with.

Most significantly, the last two years saw no extended periods of significant declines.

In 2023, the largest decline was -10% between July and October. In 2024, the worst was a 21-day decline of only -8% between July and August.

While this was a welcome respite from the normal market rhythm, the financial media would likely have been dismayed! More seriously, there’s a danger that investors will forget the important lessons learnt from past declines.

To prepare you for the possibility of more significant declines in the coming year, we outline a few points below that you should keep in mind when others are losing theirs.

What You Should Know

It is a feature of the stock market that values do not move in a straight line but instead fluctuate around a generally upward trend. We refer to this as “volatility.”

A market correction is defined as a 10% drawdown from a previous market high. While it may sound like a significant number, these events occur far more frequently than most investors believe. Indeed, they come around as often as your birthday, with years like 2024 being the exception.

Since the turn of the century, the average annual decline has been approximately -16%. While this may surprise you, it’s worth noting that about three in four years still ended with a positive return.

We also know from market history that we expect a decline of more than -30% approximately every five years (on average), as we last experienced in 2020.

How You Should React

We know that stock markets generally provide positive returns about three in every four years. The one negative year is what earns you the other three positive years. It’s the price of admission for profiting from the collective ingenuity of the hundreds of companies working for you while you sleep. We encourage you to see the temporary declines as the reason for the stock market’s permanent returns. You can’t have one without the other.

Unfortunately, we cannot consistently predict when these fluctuations will occur or when they will reverse. To be a successful long-term investor, one must accept this with humility.

Market declines will consistently occur throughout your investing life, and your mindset during these times is a choice that will shape your financial future. We advise you to confront them with confidence rather than fear while being mindful of the opportunities they present.

Time Heals

Ultimately, what happens in the next year is relatively unimportant to your 30-year plans. If you’re investing long-term, the odds are stacked in your favour. You’re guaranteed to win.

After two years of little volatility, if we experience a decline in the coming months, be encouraged that you are busy earning future returns. Additionally, if you’re still saving, declines are your best friend, allowing you to buy more units of shares at reduced prices.

While we don’t know where the market will be at the end of 2025, we’re pretty confident about where it will be in 10 years: much higher. Time is the enemy of market declines, and most investors have plenty of time.

Difficult Conversations - the heart of financial guidance

For many years, the role of a financial adviser was limited to providing access to financial products, often acting more as an order-taker than an advice-giver.

However, in an era where financial information is at our fingertips and financial products are readily available, our role has had to evolve significantly.

Today, the best advisers act as thinking partners and professional advisers to help families achieve their most cherished financial and life goals. We are committed to this new way of being and see ourselves as partners in your financial journey, dedicated to guiding you towards a secure future.

Like any meaningful relationship, this partnership thrives on mutual respect, trust, and honesty.

Short-Term Discomfort, Long-Term Gain

While it's easy to maintain this honesty when you’re on track with their financial goals, true partnership shines brightest during challenging times. When it becomes apparent that you may be veering off course from their financial objectives, our commitment to honesty compels us to have difficult yet crucial conversations.

We regularly encounter situations that require a difficult conversation that requires empathy. Some days, we encounter a pre-retiree who believes that investing regularly is unnecessary because retirement is decades away. On other days, we encounter retirees withdrawing unsustainably from their investments, jeopardising their long-term independence.

While uncomfortable to discuss, these scenarios require crucial conversations that can alter financial trajectories. Because financial discussions can be emotionally charged, we aim to guide clients through these conversations with sensitivity and care. If we ever need to have these conversations with you, we’re here to support you as we work together towards your financial goals.

Embracing Honesty for a Secure Tomorrow

While avoiding these topics might feel easier in the moment, if not addressed, the problem will only grow, potentially causing irreparable damage. By addressing issues early, you can make smaller, more manageable adjustments rather than drastic overhauls later.

Think of your financial journey as a flight. As your advisers, we are the co-pilots, regularly checking the instruments and suggesting course corrections. Even a slight deviation can lead you far off course over time without these adjustments. Our duty is to ensure you reach the intended destination, and course corrections are inevitable.

As we navigate your financial journey together, remember that our commitment to honesty stems from a genuine desire to see you succeed. We're not just looking at the you of today but advocating for your future self – the person who will benefit from the decisions and adjustments made now.

We are committed to being supportive partners who care enough to tell you what you need to hear, not just what you want to hear. If there’s anything we need to hear that will strengthen our relationship and the value you get from it, we encourage you to bring it up.

We encourage open dialogue. Ask us questions, share your concerns, and be receptive to feedback. This collaborative approach, built on mutual trust and respect, is the cornerstone of our mutual long-term success.

The Dividend Advantage

One of the most commonly misunderstood aspects of investing is what it really means to be an equity investor. For many investors, it brings up thoughts of a casino, where some are lucky enough to win, but most end up on the wrong side of the “house”.

However, mature investors understand that when you invest in the great companies of the world, you're not just buying an invisible item– you're becoming a part-owner in real companies that sell real products and services to real people.

The long-term financial rewards of being an equity investor are twofold. The first is the hope of one day selling your shares for more than you bought them. This becomes a real possibility when the company improves its profits over time, either by selling more goods and services or passing on inflationary input prices to consumers.

The second is the hope that the company’s management will distribute a portion of annual profits to equity owners as a cash dividend.

Understanding dividends reinforces a crucial point: As an equity shareholder, you're not just speculating on stock prices – you're participating in the financial success of actual businesses. Let’s explore this aspect of equity ownership further.

The Dividend Decision: Spend or Reinvest?

As a dividend-receiving investor, you face a key decision: what to do with these payments?

The first option is to receive the dividends as cash. This can provide a regular income stream, which might be attractive if you're looking to supplement your current lifestyle or invest in other opportunities. It's an immediate win – cash in hand that you can use as you see fit.

The second option is to purchase additional shares of the same stock or fund. This approach continuously increases your ownership stake.

While receiving cash dividends offers immediate gratification, reinvesting sets the stage for potential long-term growth. By reinvesting, you're buying more of an investment strategy you already believe in without investing additional money from your pocket.

The Compounding Effect

The decision to reinvest dividends can profoundly impact your long-term financial outcomes, thanks to the power of compound growth. When you reinvest dividends, you're not just earning returns on your initial investment – you're earning returns on your returns.

Let's look at some numbers to illustrate this point. Historically, reinvesting dividends has accounted for a significant portion of the stock market's total return. For example, $100 invested in the MSCI World Index in 1999 grew to $310 by the middle of 2024. However, with dividends reinvested, your investment would be worth $557.

It's important to understand that the share prices or index levels, as reported in the financial media, often exclude dividends. If you reinvest dividends, your actual returns could be substantially higher than these numbers suggest.

This "hidden" growth through dividend reinvestment can dramatically accelerate your journey to financial independence. It's a powerful force that, over time, can turn even modest investments into significant wealth.

Harnessing Dividend Power

Understanding and appreciating the true nature of being an equity investor is the foundation of long-term investing success.

As far as possible, we urge investors to seek out funds or platforms that offer automatic dividend reinvestment. Implementing the appropriate strategy for you in this way will make it easy to put your dividend strategy on autopilot.

As your financial advisers, we’re here to help you navigate these decisions and implement an investment strategy that aligns with your long-term financial goals. With our help, we hope you can make informed decisions that align with your unique goals and circumstances.

The inevitable outcome for those harnessing this power of compound growth is financial independence and a dignified retirement.

The cumbersome nature of modern financial housekeeping

Financial planning has made significant strides over the past few decades, giving today’s investors advantages that would have been unimaginable to previous generations.

Access to caring financial advisers available online, low-cost investment administration options, digital signature capabilities, easy account aggregation software, and global equity portfolios with no upfront fees are just some advancements that have become commonplace.

Technological advancements have streamlined even the most complex financial tasks, allowing for more efficient personal financial management. Implementing a financial strategy in a sensible and cost-efficient manner is easier than ever.

The Growing Tangle of Financial Administration

Despite these advancements, investors increasingly face a growing burden of financial administration and housekeeping. Though driven by well-meaning consumer protection measures, this proliferation has become counterproductive. The sheer volume of paperwork and compliance requirements can often feel like a full-time job, overwhelming even the most organised investors.

An anecdote that aptly illustrates this trend is a parent recently being required to complete a risk assessment questionnaire for their three-year-old child. This isn't just a quirky story; it symbolises the sometimes absurd and often frustrating world of financial administration that has been thrust upon us.

From annual "Know Your Customer" (KYC) updates to the complex "source of wealth" forms demanded by banks, the complexity of these tasks is skyrocketing. Much of it feels disconnected from our real lives, as the questions asked often miss the mark, failing to capture the nuances of an investor’s true situation or understanding of the market.

A Light in the Maze

Worryingly, this trend is deeply embedded in our financial ecosystem, growing denser each year, and we are concerned that most investors are not equipped to navigate this maze.

The caring financial adviser can play a significant role in helping consumers navigate this tangle of forms, procedures, and endless requests for information. While it’s not our primary role, we alleviate the anxiety that comes with this burden in three ways.

First, we help clients make sense of the administrative minefield. We cut through the underbrush of paperwork and procedures, providing a clear path for clients to follow. Knowing what’s being asked is often half the battle, and we understand the landscape better than most.

Second, we protect clients from the increasing number of phishing attempts designed to defraud unsuspecting victims. Financial scams are increasing, and elderly, retired investors are often targeted.

Third, we assist clients in completing the necessary tasks, often removing many unnecessary requests from their plates altogether.

From Chaos to Clarity

While personal finance has seen remarkable advances, the escalating complexity of financial administration can sometimes overshadow these benefits. This complexity can make the financial landscape seem more like a labyrinth than a clear path to financial security.

We are your guides in all financial matters, ready to assist when needed. Though some financial housekeeping is unavoidable, today’s burdens can be navigated more efficiently with our help.

By showing you the simplest way through this maze, we hope to give you more time to focus on what matters most to you and your family. Our ultimate goal is to ensure that you can enjoy the benefits of modern financial advancements without being overwhelmed by administrative duties.

The allure of ‘more’

Cashflow is the lifeblood of any financial plan. How we allocate the money coming in will determine both the present and the future of our families. It’s not a glamorous topic, but it’s undeniably ground zero of financial success.

Our cashflow challenges evolve as we move through the different life phases. Our early working years are typically about providing for essential daily “needs”. For those whose careers allow them to break free from daily concerns, the allure of certain “wants” starts to emerge. These desires challenge our beliefs about what we need to be happy.

This internal battle rages on throughout life, and how we respond to this challenge will determine our future financial success. But what truly brings fulfilment, and what consequences do these decisions have for our future selves?

The Quicksand of Accumulation

Our desire to accumulate more is grounded in evolution. A striving for “more” drove past generations to create the world we now live in, and current-day economic theory is still based on the assumption that “more is better”. But, in a world where most of us have moved well beyond providing for basic needs, does this instinct for more create problems we could do without?

Embracing The Tradeoff

There are many ways that spending can bring happiness and joy – many of my clients have shifted their spending from possessions to experiences with family and loved ones.

However, everything in financial planning is a tradeoff. For many, embracing “more” comes at the expense of their own “tomorrow”.

Yet, we need the balance to not miss out on today for a tomorrow that might never come.

Before all of us lies the invitation to let go of pursuing “more”, choosing instead to embrace “enough”. We appreciate and understand that everyone’s definition of satisfaction and “enough” is unique and personal.

The other week I had back to back meetings with retirees - the amount they spent on a monthly basis was greatly different to each other. Yet both were incredibly happy.

Each persons Enough will be different.

Navigating Together

While you will always remain the expert in the design of your own life, my job is to be the expert in guiding families in making the tradeoffs that provide them both meaning in the present and an independent future.

Guiding families from pursuing “more” to embracing “enough for tomorrow” is our reason for being. The comprehensive planning we provide includes all the tools you need to walk your financial journey successfully. We look forward to guiding you on your journey to “enough”.

Longevity - the underappreciated risk

There are two distinct stages in an investor’s financial planning lifetime.

The first requires them to squirrel away money for the future, hoping to benefit from the magic of compounding returns. We call this the “savings stage”.

At retirement, the investor transitions to the “spending stage” of life. From this point, they will withdraw from, rather than continue adding to, their investment portfolio. While any habit of frugality they developed during their life will continue to be beneficial, this major change in direction can be a difficult adjustment.

In this phase of life, we’ve identified two risks facing the retired investor: one risk we believe they fear a little too much, and the other risk we see them fear not enough. We’ll unpack both risks and highlight why the one deserves more attention.

The Eternal Fear – Volatility

Like the pre-retirement investor, retirees also have an innate fear of market declines. These are periods when market prices decline, often due to a global crisis or worsening economic fundamentals.

The technical term this has become known by is “volatility” – the erratic fluctuations of market values around a typically rising baseline. In essence, the takeaway for the investor is that while the market has historically risen, it does so not in a straight line.

The fear for the retiree is that while the market is experiencing a temporary decline, they will need to sell investment units at a lower price to fund their living expenses. This, all other things being equal, does have an impact on the expected lifetime of their assets. It’s a factor that should be considered, but it can also be planned for.

For example, many retired investors retain a lump sum in cash, from which they can make income drawings during times of market decline.

The reality is that temporary declines happen regularly without warning. The best way to earn the full market returns is to endure these periods with patience and discipline. By planning properly, we can essentially shield an investor from permanent damage happening from temporary declines.

The Underappreciated Fear – Longevity

Over the last few decades, the average investor's life expectancy has significantly increased. A few generations ago, it was rare for a retiree to live for longer than fifteen years while relying on their investment assets. Today, thanks to advancements in medical care, diets, and healthier lifestyles, a retired couple has a one-in-three chance of one of them living to age 95.

For the average retiree, that is over three decades of living expenses, medical care, and unexpected emergencies that need to be funded by their pensions and investment assets. From experience, the typical retiree vastly underestimates the risk that this poses to them in their quest to remain financially independent. The investment decisions they will need to make to provide for this period will require them to put aside other fears, such as the innate fear of market declines, to give them the best chance of success.

The goal is three decades of a rising, inflation-cancelling income. The risk is that they focus on short-term fears that disadvantage them in the long term.

A Changing Landscape

The shift in focus that increasing longevity brings into play will impact the mindsets, approaches, and rules of thumb that retirees have become used to. This stresses the importance of a comprehensive retirement income plan built on evidence and rigour.

Additionally, those who are still firmly in the “savings stage” will need to adjust their expectations for what the appropriate amount is to save for their future selves. It’s a changing world, and no one is safe from the need to adapt.

As the world continues to evolve in various ways, we encourage you to consider how this impacts the way you are providing for your own future. Our financial planning philosophy will always emphasise regular reviews, and in this way we hope to make sure that our clients are always prepared for changes that others are yet to identify. Ready to start your journey?

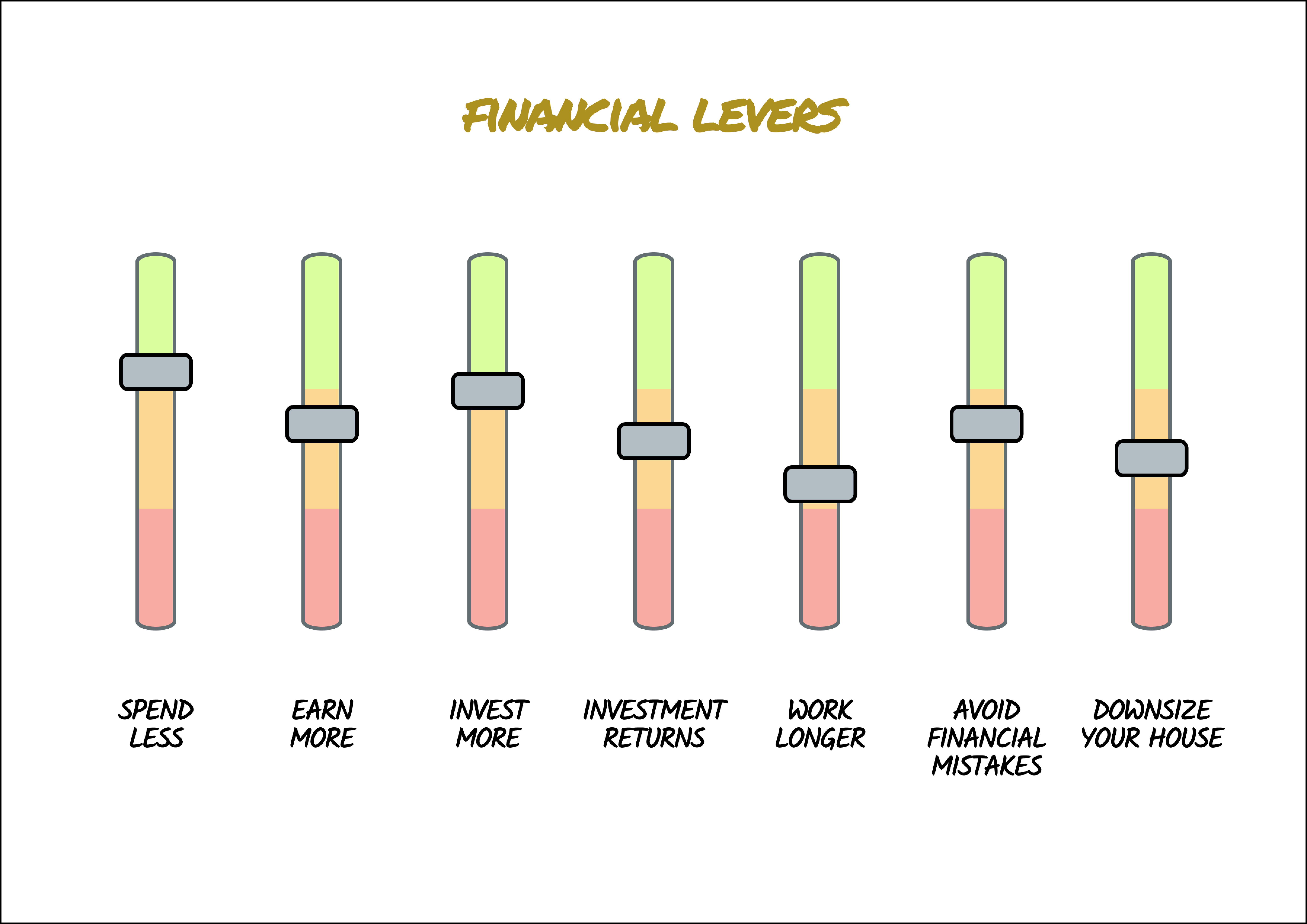

Your Financial Levers

When managing money and working towards financial goals, it's important to understand which factors we can control and which we can’t.

Interest rates, inflation, investment market returns, and economic growth fall outside our control. However, there are many factors we can control, and each of these becomes a lever we can pull to adjust our future financial circumstances.

In this article, we will explore the various financial levers that investors can utilise to enhance their financial well-being and achieve their desired outcomes.

Controlling Expenses

One of the most powerful levers at our disposal is the ability to control our expenses. It's vital to assess our lifestyle choices and avoid falling into the ‘lifestyle creep’ trap, where we progressively increase our spending as our income rises.

How mindful are you of your spending habits? By spending less and living within our means, we can free up resources for savings and investments.

Increasing Income

Another financial lever that investors can pull is increasing their income. While this may seem obvious, many individuals underestimate its potential. We can accelerate our wealth-building journey by actively seeking ways to earn more through career advancement, side hustles, or entrepreneurial ventures. Increasing our income provides us with more resources to save and invest, expands our financial opportunities, and enhances our financial security.

Investing More

Investing more is a powerful lever that can significantly impact our long-term financial success. By allocating a larger portion of our income towards investments, we can capitalise on the power of compounding and benefit from the growth potential of various asset classes. Adopting a disciplined approach to investing, such as automatic savings and paying ourselves first, is crucial. By consistently investing over time, we can build an investment portfolio that aligns with our financial goals.

Enhancing Investment Returns

While controlling expenses, increasing income, and investing more are essential, investors should also focus on enhancing their investment returns. This lever involves making informed decisions about asset allocation and diversification, and selecting investments that align with our long-term objectives. While investment returns alone should not be relied upon as the primary driver of financial success, optimising our investment strategy and seeking opportunities to maximise returns can significantly impact our overall wealth accumulation.

Adjusting Retirement Timeline

One often overlooked financial lever is adjusting our retirement timeline. While many individuals plan to retire at a specific age, it's important to re-evaluate this timeline based on our financial situation and goals. Extending our working years can give us additional time to save and invest, allowing our assets to grow further. On the other hand, some individuals may choose to retire earlier, focusing on achieving financial independence and creating a fulfilling lifestyle. By carefully considering our retirement timeline, we can make informed decisions that align with our unique circumstances.

Avoiding Financial Mistakes

Avoiding financial mistakes is critical to protecting our wealth and financial well-being. By being vigilant and educated about common financial pitfalls, we can mitigate risks and preserve our financial resources. Learning from our mistakes and seeking wisdom from experienced individuals can help us navigate the complex landscape of personal finance and make sound financial decisions.

Housing Considerations

Housing decisions can also serve as a financial lever. Right-sizing or downsizing our house can release equity and reduce housing-related expenses, freeing up resources for savings and investments. Additionally, exploring innovative options like equity release can provide additional financial flexibility without the need to move house. We can optimise our housing decisions to align with our broader financial goals by carefully evaluating our housing needs and considering the financial implications.

Empowering Your Path to Financial Success

In summary, investors have a range of powerful financial levers to take control of their financial situation. Pulling these levers consistently over time can compound to create life-changing results.

However, working with a qualified financial adviser can provide invaluable guidance in adjusting these levers to match your specific circumstances and financial goals. By understanding these levers and collaborating with a financial adviser on how to pull them, investors put themselves in the best position to choose their financial path and progress steadily towards their definition of financial success.

A beauty in simplicity

As we grow up and experience more of the world we learn that a topic typically gets more complicated as we dive deeper into it.

For example, supply and demand is a concept most of us can grasp quickly, but having a deep understanding of how these variables are affected by changes in interest rates, inflation and trade relations requires further study.

We also find that for those who push past a certain point in any discipline things seem to simplify again. The detail fades away, you unlearn some of the complexities that don't seem to matter, and you're able to distil the subject into the few key points that really matter.

True simplicity comes from a deep understanding and appreciation for the subject matter. When shared, this simplicity allows the rest of us to make sense of the world without becoming an expert in every field.

Every great teacher or writer has this quality. Richard Feynman's writing can make anyone appreciate the key lessons in physics, and he'll make you laugh. Who would have thought physics could be humorous?

Complexity For Its Own Sake

Unfortunately, we too often encounter complexity where simplicity is what we really need. In many cases it's used as a way to confuse, leaving the recipient with little understanding and keeping them reliant on the expert.

The financial industry is no different. Experts highlight the dismal level of financial literacy and argue for financial education to be part of the school curriculum, but very few contribute to the changes we need.

Most industry players are complicit by using complexity to spread fear and a reliance on an industry which is happy to sell a product without having the buyer understand what they are getting themselves into.

The media creates the crisis of the day (or fans the flames) while the financial machine stands ready with the solution which would have solved the previous crisis but little chance of being suitable for the current challenge.

If there's anything we've learnt from the history of the financial markets it's that there are a few key learnings which will always apply. Once you approach every new crisis with this knowledge, the world becomes much simpler.

Simple Is Better

Money, too, can be simple if you want it to be.

If it's complexity you want, then financial product providers will give it to you. There's a product for every financial fear you might have. But starting here is likely to lead you astray. You'll need to work out what these mean for you and the lifestyle you want to have. A new crisis might make you second-guess your tactic, taking you back to square one.

A true understanding of money allows you to build on your understanding of your own situation and the life you want to live.

A strategy can then be built on a simple understanding of the concepts of spending less than you earn, investing for your unknown future, providing for short term expenses, compound interest, and historical market returns combined with old-fashioned discipline and patience.

We have found that people find the above process easier when it's facilitated by a caring financial adviser who can educate, encourage, and hold them accountable.

Products may be required, but they'll be put in their rightful place.

The Choice Is Yours

We have a choice between simple and complex in many areas of life. Sadly, complexity is often perceived as clever and sophisticated. It's easy to look down on a simple strategy when a complex one will make you look smart. With financial matters, nothing could be further from the truth.

The real tragedy is that many don't know that simplicity with money is an option. They accept the complicity sold to them with the result often being overwhelm and a lack of understanding. In many cases this leads to disengagement, which itself compounds into long term consequences.

Our experience is that simple and done is almost better than complex and perfect. Clients taking action and engaging in their own financial affairs leads to a proper understanding of how their decisions will impact their long term future

How can your plan be simplified to remove the unnecessary?

The active mess

Australian investors throw away millions of dollars each year using funds with active fund managers.

An actively managed fund involves a fund manager buying and selling stocks and shares in an attempt to outperform the market they’re operating in - such as the Australian or international share markets.

However, research company PIVA monitors these funds and annually produces reports chronicling if any of these managers manage to beat their targets.

As you’ll see in the above chart, in the Australian share market sector in year one nearly 60% fail this test. And as the years go on that number increases.

For international shares the results are even worse. In fact, over 10 years 90% of fund manages fail to beat the basic benchmark.

So why do people keep using them? Firstly, there’s some huge fees and advertising in play here. Secondly, humans instinctively follow trends and a fund that may have outperformed in year 1, will see an inflow of money from people jumping on. Years 2, 3 and 4 might be a disaster and the money drips away and in many cases the fund shuts down.

We don’t use active fund managers at Metric Wealth. That means we aren’t gifted their private lunches, drinks parties and sports tickets, passed out to those that recommend their funds - and we’re ok with that.

Our funds are highly diversified, low cost, purchasing every stock on the market - some of those companies will do poorly but they’ll be overshadowed by those that do well. There’s no guessing, no gut feel and no guesswork - it’s boring and it works. And we’re ok with that.

A Patchwork Quilt

Want to understand this patchwork quilt?

It's the rankings of different global equity markets on a year by year basis.

Australia (the aqua green colour box) was the best region to hold stocks and shares last year (despite still making a -1.1% return.)

But that's rarely been the case. And there's no way of knowing which region will be best next year.

But diversifying your savings across the world would get you constantly in the top half.

Don't look for the needle in the haystack - buy the haystack.

Rational Optimism

It is difficult, if not impossible to make a good investor out of a natural pessimist.

Investment success is based on an continual long term optimism.

Not a one-eyed optimism that says everything will be perfect along the way - it will not, there will be challenges - but a rationality that whatever the problem-du-jour: inflation, war, unemployment.... that marks the front of our news pages today, shall be overcome at some point in the future.

It has done in the past and shall be in the future.

Human progress and problem solving is inevitable but we cannot time or control it. Instead, seek advice around the areas you can control, to negate your own blindspots, from those who are rationally optimistic.

Round It Up

I heard today that around 75% of Australian's never leave tips at restaurants. I appreciate it's not as ingrained as other countries here but that still surprised me.

If you've had good service anywhere at the moment, times are really tight for anyone in the industry. If you're lucky enough to be able to still regularly enjoy the great restaurants and cafes of our area, then tip well.

There's nothing wrong with rounding up your bill at any local business, not just where you eat or drink.

Paying it forward benefits all parties. It'll brighten your day as much as the receiver.

Full House

Full house for the The Sydney Morning Herald today - almost every headline on the front page using negative language: Crisis, Loss, Failures, Battles, Fears…

Negative news sells - it’s entertainment.

Negative headlines online collect 3x the clicks of positive stories.

Shutting out the noise helps our clients plan effectively for successful lives.

Let’s focus on the top left and the 20 Best Bars